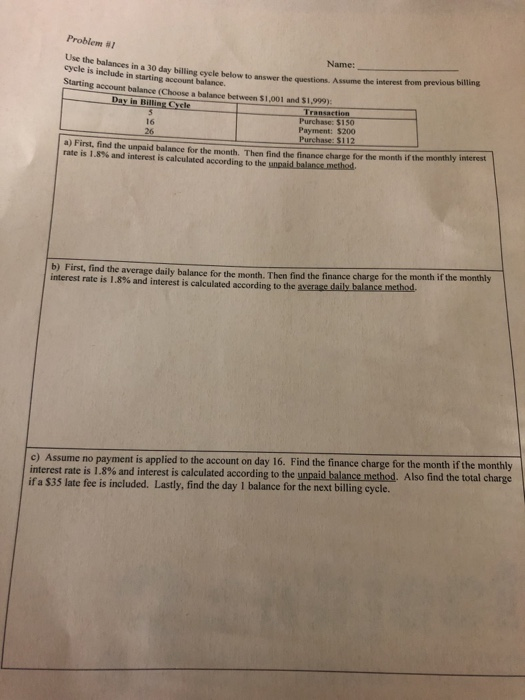

Investors looking at cost of timeshares purchasing into a business have various options, but if you invest one company, you can't invest that very same cash in another. So the discount rate reflects the difficulty rate for a financial investment to be worth it to you vs. another business. Following on point number 3, the discount rate for worth financiers is your desired rate of go back to be made up for the danger. The part that journeys up lots of people is this: "While discount rates certainly matter in DCF appraisal, they don't matter as much as a lot of experts think they do." Aswath Damodaran Because if you actively consider how you use discount rates day-to-day, you will find that you utilize them like a yardstick for your rate of return.

That something is a rate of return. Nobody and no company provides or invests cash without weighing what the returns will be or comparing it versus some other type of financial investment return. Banks provide cash to people at various interest rates depending upon the financial danger profile. I purchase the stock exchange ready to take on more risk than a cost savings account or a guaranteed treasury bond, for a rate of return going beyond both. The value of any stock, bond or service today is figured out by the money inflows and outflows discounted at a suitable rate of interest that can be anticipated to take place during the remaining life of the asset.

This is a lot of talk on, so let's make it more practical. To see how discount rate rates work, compute the future value of a business by forecasting its future cash generation and then including the overall sum of the cash created throughout the life of business. This needs you to compute a growth rate and after that apply it to the business's totally free capital. To show, let's assume a business's financial filing revealed $100 in totally free money this year. With a growth rate of 10%, the company will have the ability to create $110 in totally free cash next year and $121 the year after and so on for the next ten years.

1 $110 2 $121 3 $133 4 $146 5 $161 6 $177 7 $195 8 $214 9 $236 10 $259 $1,753 But the amount of $1,753 over ten years is not worth $1,753 today - What do you need to finance a car. If you had the option of receiving a total amount of $1,753 expanded over ten years or $1,753 in one lump amount today, which would you pick? The single up-front payment, naturally. Before I discuss why, let me show you: 1 $110. 91 $100 2 $121. 83 $100 3 $133. 75 $100 4 $146. 68 $100 5 $161. 62 $100 6 $177.

51 $100 8 $214. 47 $100 9 $236. 42 $100 10 $259. 39 $100 $1,753 $1000 Getting $1,753 paid out over ten years is worth the exact same as having $1,000 today (assuming your personal discount rate is 10%). Does that make sense? Another way to put it is, if I give you $1000 today, I anticipate to be paid $110 in one year, $121 in 2 years, and so on for ten years, to timeshare team satisfy my internal necessary rate of return of 10%. That's since of the time worth of money. You understand intuitively that a dollar today is worth more than a dollar a year from now.

Not known Facts About How Is Python Used In Finance

02 in a mcdowell and company year for it to simply have the very same buying power (2% inflation rate). However no one wants to simply have the exact same quantity of cash next year you wish to make a return on it! If you invested in the stock exchange, you could turn that $1 into $1. 10 or $1. 30. A dollar next year is no great to you, since you've lost on a year of releasing it to make additional returns. This is the opportunity cost of your capital. The last reason a dollar in the future is worth less than one today is because a dollar in your hand now is ensured, however a future payment constantly has some unpredictability. Why are you interested in finance.

30 in the stock exchange, it might become $0. 80 in a bad year. That risk likewise needs to be built into your needed difficulty rate of return. The point is, you require to discount the future money flows of business you're investing in, due to the fact that money in the future is worth less than money today. And the discount rate you pick should be based upon the rate of return you require for your investment, which is normally a function of both the uncertainty of the financial investment and what else you can buy. In case you're questioning how to calculate the discount consider the above table, well, it's carefully associated to determining the development rate at period t.

If you desire to compute your own affordable money circulations, you'll need this (Which of these arguments might be used by someone who supports strict campaign finance laws?). But you don't actually need this for finding out what your personal financier discount rate need to be. As a daily financier, you do not need to utilize intricate inputs and designs. I confess my method is far from best. However it gets much better each year as I continue to fine-tune my approach. Prof Damodaran supplies remarkable tips and has actually composed a fantastic piece on corresponding. Consistency: a DCF first concept is that your cash flows need to be defined in the exact same terms and unit as your discount rate.

/dotdash_Final_Risk_Feb_2020-01-66f3c5ffb3c040848f1708091fa40eb9.jpg)

A discounted money circulation assessment needs presumptions about all 3 variables however for it to be defensible, the assumptions that you make about these variables have to follow each other. a great appraisal links narrative to numbers. A great DCF valuation has to follow the exact same principles and the numbers have to be constant with the story that you are informing about a company's future and the story that you are informing has to be plausible, given the macroeconomic environment you are forecasting, the market or markets that the company operates in and the competition it faces. Not as easy as it looks, however not as hard as it appears.

Probably you will utilize FCF as the capital. It is the most common worth you'll encounter and one that is easy for value financiers. FCF is post-tax and not changed for inflation (real, not small value). For that reason, the discount rate should also be considered post-tax. E.g., if you like to use 10% returns in your estimations, you are most likely thinking of a 10% pre-tax return. If you do desire a 10% return post-tax, then your pre-tax discount rate is most likely 11. 5 to 13%. However once again, if your pre-tax wanted rate of return is 10%, then your post-tax discount rate ought to be 7 to 8.